We visited Oahu for the kids’ Spring Break Vacation. We stayed in Waikiki for 9 days as our “home base” but we drove around the island during half of our stay. For this trip, I purchased a Go City Oahu 3 day “All Inclusive” pass. I bought 2 adult and 2 child tickets.

Kualoa Regional State Park – The Chinaman’s hat on the background

While planning our trip to Oahu, I know there are certain things I want to do with the kids like the Luau, Polynesian Culture Center (PCC) and a visit to Kualoa Ranch. Individual prices cost more than the Go City Pass as you will see below.

How does Go City Pass Work?

There are two types of Go City Pass. An Explorer Pass and All Inclusive Pass. The Explorer Pass let you choose the number of attractions to visit for a set amount. Once you visit your first attraction, you have 60 days to use it. This make sense if you have a specific attraction to visit in mind. The All Inclusive Pass let you visit all the attractions that Go City partnered with for a set number of days. You can pick from 1, 3, 5 or 7 days. Once you visit your first attraction, your pass is “activated”. You then have 14 days to use the pass before it expires.

All Inclusive Pass Itinerary in Oahu

We purchased 3 days All Inclusive Pass for our vacation. This all inclusive pass includes a “Premier Attraction” which is only available for all inclusive option. Our itinerary looked like these.

Day 1 – Travel Day

Day 2 – We used our Go City Pass to visit Kualoa Ranch. We did an early Grown Farm Tour. In the afternoon we visited the Polynesian Culture Center

Cost of Individual Tickets for 2 adults and 2 kids: $551.72

Go Pass Tickets: $814.14

Day 3 – Beach Day in Waikiki

Day 4 – We took a Catamaran Tour in the morning and a Luau in the evening

Cost of Individual Tickets for 2 adults and 2 kids: $982

Go Pass Tickets: $0

Day 5: Beach Day in Ko’Olina

Ko’Olina Beach Lagoon

Day 6: Secret Island Tour in Kualoa Ranch

Cost of Individual Tickets for 2 adults and 2 kids: $198.74

Go Pass Tickets: $0

Day 7 and Day 8 – Beach Day and a stroll in Waikiki

Day 9 – Travel Day

The total cost for individual tickets were $1,732.46 while the Go City passes were $814.14. Our savings were $918.32.

We could have save more by visiting more attractions, but with 2 kids, we like to lay low and stick to a couple of attractions per day.

The Go City Pass is vary easy to use. Go City Pass will ask you to download the app and redeem your tickets. Once redeemed, it will show your QR Codes. I took a screenshot of the QR code and saved it on my photo so it is easy for me to find. Once activated, it will also show you the expiration date. The expiration date is the 14th day once you activated your pass.

Go City Typically have sales going on ALL THE TIME. During the time I bought my pass, Undercover Tourist is the cheapest. You can also check out Groupon because they sell it as well.

Overall, I recommend using Go City. You have to plan ahead, but it can be totally worth it with some big savings in the end!

March brought us the start of spring. These are the days that makes it worth it to live here in the Pacific Northwest. We might endure the long and gloomy days but the gorgeous days like the ones we have in March totally make up for it. We have more appreciation of nice weather and we were outside as much as we can utilizing our neighborhood playgrounds.

The beautiful mountain

This month, MBP was invited to a birthday party with his friends at an arcade/bowling place. The kids got some cards to play with the arcade for a couple of hours, pizza and cake. We also went to a local high school for “Easter Egg”. The kids saw the Easter Bunny and some princesses.

Our tulips are almost there

This month, we spent $3,912.8. Another month under $4k, which is good. Let’s take a look.

Description

Amount

Groceries

823.92

Healthcare/Medical

538.63

Automotive

447

Education

323

Utilities

306.99

Kids Activities

293.34

Home Improvement

289.14

General Merchandise

203.52

Charitable Giving

200

Alcohol

110.3

Dues & Subscriptions

104.21

HOA

84

Restaurants

69.68

Clothing/Shoes

33

Gasoline/Fuel

26.58

Gifts

20.13

Mobile Phone

17.2

Pets/Pet Care

14.16

Travel

8

Total

3912.8

Groceries – $823.92

Our grocery spending in February was low, so this probably average out with 2 months. We didn’t buy anything out of ordinary this month. We still shop at WINCO and Costco and hardly price compare.

Healthcare/Medical – 538.63

Mr. MMD got a new retainer. This is specifically fit him by his dentist. It cost $450. He also paid $50 deductible for his last dental cleaning. I paid $5 for my vision insurance and $33.63 for some lab exams. We paid our health insurance through a gift card by having enough rewards from preventative care. Our dental insurance was paid February.

Automotive – $447

I switched from Geico to Progressive. The last bill from Geico was $673.37 for the same policy. We saved over $200 by getting other quotes. I thought about getting our insurance from Lemonade which charge you a “per mile” insurance. We might go camping this summer and might drive more. I ended up signing up for Progressive. The bill is the 6 month insurance for our 2011 Toyota Prius and 2011 Volkswagen Jetta. We only have liability and personal injury protection.

Education – $323

AHP’s preschool tuition. He goes 5 days a week for 3 hours.

Utilities – $306

Our electric and gas were $181.72. This should go down as the weather warms up. Our sewer is flat at $69.41 and water bill was $55.86.

Kids Activities – $293

I signed up MBP for a summer camp for a week this coming summer. We like to stay local to enjoy the glorious weather here in the Pacific Northwest, but it will be good for him to go to some camp at least for a week. I also got some stuff for easter from the dollar store for $19.16. We got the kiddos some items from the Scholastic Book Fair for $13 and lastly, we got MBP’s class some items requested by his teacher for $11.18.

Home Improvement – $289

Some more items for the yard, some wood for another planter and some plants from Costco.

General Merchandise – $203.52

Catch all from Costco and Amazon. These are items like toilet paper, paper towels, new pan or anything that we don’t want to categorize.

Charitable Giving – $200

Church offering for March. Both MBP and AHP joined me to church on some Sundays. They get a choice if they want to go. Sometimes they do, but sometimes they don’t.

Alcohol – $110

A wine for my book club and Mr. MMD’s liquor and beer from Costco.

Dues and Subscription – $104.21

I signed up for a year of ad-free HBO max. They are having a sale and I was able to avail a $25 statement credit from Chase. Total for the year were $89.96. Our Amazon prime were $7.65. I also paid for a month of Paramount Plus. I forgot to cancelled my free subscription.

HOA – $84

Our HOA fee to maintain the 20+ miles of trails and numerous playgrounds in our neighborhood. I’m still not a fan of HOA, but we uses the trail almost every day to go to school. We also definitely enjoy the playgrounds.

One of the playgrounds

Restaurants – $69

We went to our local Diner after the easter egg hunt. The kiddos also visited the same place for some milkshakes on one sunny Saturday. Included here as well were MBP’s hot lunches for school. We started letting him having hot lunches from school once a month. I put in $11.25 on his account. This is about 3 lunches.

Clothing – $33

I got MBP new shoes from REI, which we might return. I’m still not sure.

Gas – $26.58

One tank of gas for our Prius.

Gifts – $20.13

A gift for MBP’s friend for his birthday.

Mobile Phone – $17.2

A gig of data for 2 lines from Xfinity Mobile. I just received an e-mail that this will increase soon.

Pets – $14.16

Our furbaby’s compostable poop bag.

Travel – $8

Deposit for our Catamaran Tour and Kualoa Ranch Tour for our trip to Hawaii.

Another month had passed and we are slowly starting to get out of the gloomy season. This month, we celebrated Valentine’s Day, AHP’s 4th Birthday and MBP’s first time selling Campfire Candies.

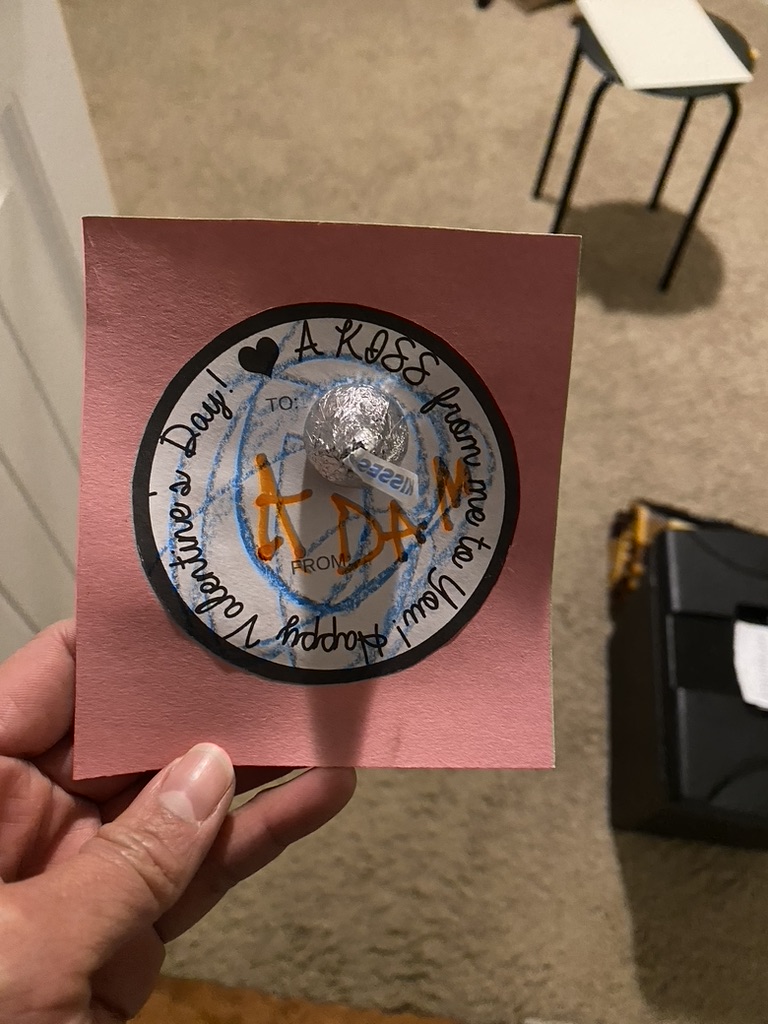

Valentine’s Day is a big day at the kid’s school. This day is basically all about them now, with all the hearts, sweets and classroom celebration. The boys handed out some Valentine’s Day cards for their classmates. I printed out some Valentines Day Cards at home glue it on a construction paper. AHP wrote his name and MBP addressed 24 cards for his classmates. I have to bribe AHP to write his name and hold the maker correctly. There were some tears involve doing his cards. The boys got a ton of kisses from Christmas. I taped one per card. The kids came back home with more sweets and they are not even done with their Christmas Candy.

Kid’s V-Day Cards

The next day was AHP’s 4th birthday. He was so excited! We brought some donuts to his school per his request and had a celebration at home that weekend. I went to the dollar store and got him some balloons and a couple of truck for his birthday gift. The balloon was such a hit! I have to keep reminding them to take turns. It was a solid effort for them. The boys helped me make some cupcakes for the weekend celebration. MBP got a new marble run, some more cars and $$$.

I helped decorate MBP’s room

We also got busy with the annual fundraising for Campfire. MBP sold some candies. He sold quite a bit of boxes at the grocery store. We also went door to door here in our neighborhood. His goal was to sell 45 boxes of candy and he ended up selling 125. He was very upbeat in the grocery store and wasn’t bother with some rejects. He had fun, but I’m glad its over.

AHP’s B-day

We also had a long weekend to celebrate the Presidents Day and I continued preparing taxes for VITA. I also completed ours and my brother’s tax returns. We got another refund this year, mainly because of the energy rebate for our heat pump.

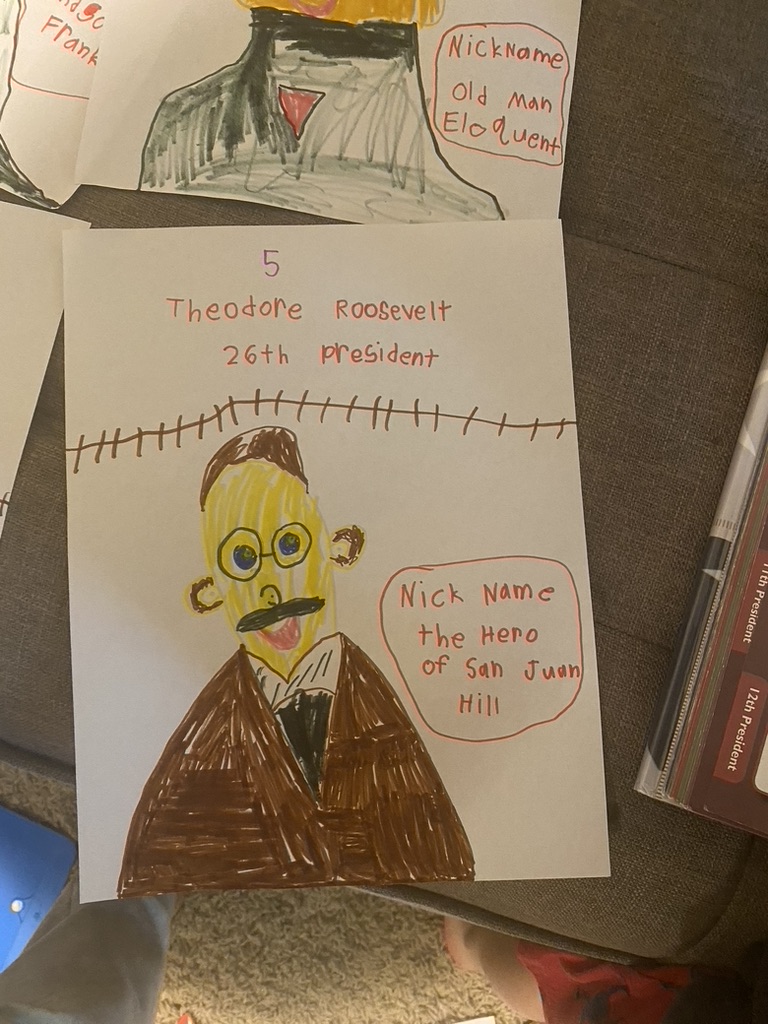

MBP’s President Portrait

Our spending is the lowest at $1,957.64. I’m pretty sure that the last time we spent under $2k was during the pandemic. I’m just seeing this now too, so let’s take a look at our spending.

Desrcription

Amount

Groceries

550.76

Utilities

346.92

Education

323

Kids Activities

157.33

Home Improvement

93.38

General Merchandise

86.86

HOA

84

Gasoline/Fuel

70.14

Clothing/Shoes

68.98

Healthcare/Medical

64.01

Restaurants

45.71

Internet

26.44

Mobile Phone

17.2

Dues & Subscriptions

7.65

Gifts

6.02

Hobbies

5.24

Travel

4

Total

1957.64

Groceries – $550.76

It’s low, probably because there’s less days in February. Nothing unusual here aside from the Girl Scout Thin Mint Cookies. I bought 3 boxes from the girls that knock on our door. Cookies are now $6 per box, just like our Campfire candies.

Utilities – $346.92

Our electric and gas was $142.14. It was a bit higher because it was cold. Our garbage was $81.24. Sewer is flat at $69.41 and our water bill was $54.13

Education – $323

Monthly preschool tuition for AHP.

Kids Activities – $157.33

We donated $100 for MBP’s Readathon. We also got some campfire candies ourselves. I got MBP a tennis racket and 18 tennis balls from Walmart all for $27.33. We went to our local high school tennis courts and the boys tried to hit some balls.

Going home from school

Home Improvement – $93.38

I got a dozen of solar path lights from Costco. Turned out that I don’t like it, so this will get return in March. Mr. MMD got some stuff from Lowe’s

General Merchandise – $86.86

These are catch all which includes Amazon orders, household supplies from Costco like toilet paper, paper towel, etc. I don’t really track this too much.

HOA – $84

Flat fee per month that will most likely increase next year. We do enjoy the trails and playground.

Gasoline / Fuel – $70.14

We filled up twice, one for Jetta and one for Prius

Clothing – 68.98

Mr. MMD ordered a bunch of shirts.

Healthcare/ Medical – $64.01

Dental insurance was $38.76 and my vision insurance was $5. I also got some preservative free eye drop from Costco. It was on sale and cost $20.25 for 100 vials. This should last me for at least 3 months.

Restaurants – $45.71

We went to McDonald’s once after MBP completed his Campfire Candy Sale. The donuts for AHP’s birthday were $27.41

Internet – $26.44

Xfinity has been charging me for an equipment rental. This should be lower next month.

Mobile Phone – $17.20

We are still on the same plan at Xfinity. This is for 2 lines using under 1GB per month.

Dues and Subscription – $7.65

This is for Amazon Prime. We get the most use of this through music using Alexa.

Gifts – $6.02

Dollar tree gifts for AHP.

Hobbies – $5.24

I bought the Kindle version of Fourth Wing. I found this book through the book club and got a bit obsessed with it. I probably read this book more than three times by now. I also read the 2nd book, Iron Flame. I got the book from the library.

Travel – $4

Deposit at Kualoa Ranch for our tour this upcoming Spring Break.

February has been good so far and I’m looking forward to Spring! How’s your month?

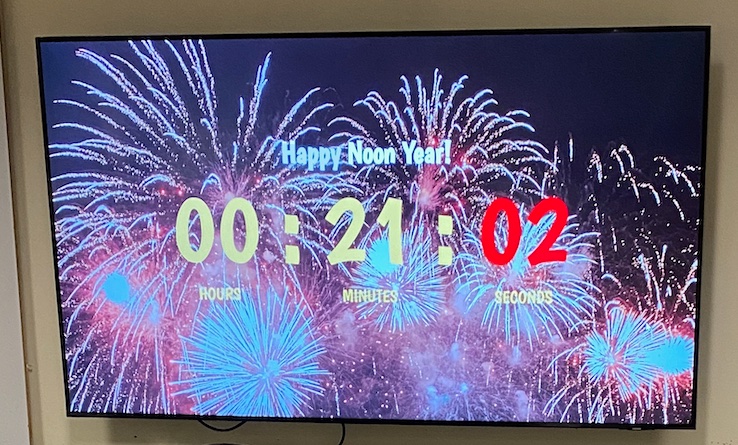

First month of the 2024 felt very long and short at the same time. We had a low key New Years Eve Celebration. Our local library had a Happy Noon Year celebration. The kids did a countdown and had some bubbly drink. It was surprisingly nice that day so we also visited our local playground. For the actual New Year’s countdown, we watched the London countdown on You Tube so AHP can see it before his bed time. We also watched the New Years countdown for MBP. For dinner, we had burgers and tots. The grown ups were also in bed before midnight. It was glorious. It is actually hard to think that I used to go out on parties for New Years pre kids.

Noon Year Countdown

The kids went back to school and I welcomed our daily walk routine. MBP now built a stamina to walk back from school. The hill was hard to begin with, but we took it slow and I’m glad that I don’t have to push the stroller from school.

I also turned 38 this month. I celebrated it with my family with a cake and a special dish request from my parents. Mr. MMD, MBP, AHP and I also went to Red Robbins for dinner. I got my free dinner. I also purchased a discounted GC from Raise right before we went. The total of our dinner out was about $10.

Birthday Breakfast

Tax season also started and I’m officially employed. I managed a tax site, preparing taxes for low income people. January was still slow, so I never worked more than 10 hours a week. The site is open 2 days a week for 4 hours. I’d say that it really is a great part time work for me.

So for January 2024, we spent $3,652. It’s been a while since we spent less than $4,000 and I was actually surprise. Let’s take a look at our spending.

DESCRIPTION

AMOUNT

Travel

901.32

Groceries

684.59

Utilities

417.14

Education

323

Healthcare/Medical

202.39

Home Improvement

202.21

Gasoline/Fuel

121.68

General Merchandise

138.22

Dues & Subscriptions

102.65

GIFT

100

Personal Care

91.19

HOA

84

Pets/Pet Care

77.32

Mobile Phone

53.2

Restaurants

49.52

Clothing/Shoes

46.64

Internet

22.87

Gym

22

Kids Activities

12.97

TOTAL

3652.91

Travel – $901

I bought four, 3 days All Inclusive Go City Pass for our Spring break trip in Oahu. The 2 adults and 2 kids price is $814.14. I bought the tickets at Undercovertourist.com and got some cash back from Rakuten. I priced out the single tickets for the attractions that we visited and we will save more than $1k by paying for the Go City Pass. Mr. MMD also got a TSA Pre check for $78. I finally had my Global Entry Interview. I paid $8 for the airport parking. Lastly, I booked our car for our Oahu trip. I used point but paid $$1.18 using my Chase Sapphire, to ensure that I get the insurance. Our trip to Oahu is set. Our airfare and hotels were all booked using points and cost us $0. I’m looking forward to this trip.

Groceries – $684

Our groceries were typical. We buy our food at WINCO and Costco. Lately, we’ve been buying some items at Walmart. I also bought a dozen spaghetti, a dozen spaghetti sauce, a couple of our wedding wine and some flowers at Trader Joes. My tax training was in Seattle, close to Trader Joes and I took the opportunity to stock up.

Flowers from Trader Joes

Utilities – $417

We had some really cold days and our electric and gas bill showed this with a spending of $214.89. Our trash bill was $81.24. Sewer was $66.46 and our water bill was $54.55.

Education – $323

This is MBP’s monthly preschool tuition expense.

Healthcare – $202

I visited an optometrist twice last January and paid $80. This is an in-network optometrist. I’m still trying to find the root cause of my sudden dry eye and unfortunately it is still on-going. I paid $38.76 for our dental insurance, $51.25 for various co-pay for lab exams. My prescription eye drop was $10. I also paid $17.38 for OTC eye drops for my dry eye. Lastly, I paid $5 for my eye insurance.

Home Improvement – $202

We installed bidets for our 2 other bathrooms. We only had it in our master bedroom, but decided that we really liked it and want to have all the toilets to have a bidet. The bidets were ordered from Tushy. I just have to write the name of the company because I think it’s genius.

Mr. MMD also have to go to Lowes to insulate our gas pipe outside. Houses in Pacific Northwest were not build for real winter condition. The weather has been changing and we are now experiencing REAL winter. The pipe froze and our furnace stopped working. Mr. MMD was able to diagnosed and fixed it. I hope that this doesn’t happen again for the rest of the winter.

The frozen pipe for our furnace

General Merchandise – $138

Various items that I don’t even bother to categorize. This is the catch all.

Gas – $121

I’ve been driving more becasue of work and training so this is for the gas of 2 cars.

Dues and Subscription – $102

My Chase Sapphire Credit Card Annual Fee was $95. This card is a keeper. We also paid $7.65 for Amazon Prime.

Gifts – $100

This was a Christmas gift for my sister. She didn’t cash the check since January.

Personal Care – $91

Mr. MMD bought a bar for our garage gym and it cost $65.69. I’ve been using it as well for strength training. I also got a haircut and paid $25.5.

Dumb bells

HOA – $84

This keeps on going up, but hey, we have a really nice trail and playgrounds.

Pets/ Petcare – $77.32

Our fur baby’s food from Chewy.

Mobile Phone – $53

We used more than 1gb of data in December.

Restaurants $49.52

Mr. MMD met up with his buddy in Seattle for dinner and Kracken Game. I purchase $50 Red Robbins GC at Raise for $15.14. I still have $9 left on the GC.

Clothing – $46

Some clothing for me, Mr. MMD and MBP.

Internet – $22

This should actually be lower since I found out that Xfinity was erroneously charging me for an equipment fee.

Gym – $22

Mr. MMD went to a pick up hockey game.

Kids Activities – $12.97

MBP’s school had a bingo party and asked for canned pet food as a donation. These are the pet foods. The event was actually pretty cool. We had chips, pizza and water. MBP won a book and was so excited when he got a Bingo!

We wrap up 2023 with some traditional and low key celebrations here at home. Although it is enticing to go elsewhere and escape the gloomy weather, we prefer to stay home and have our annual traditions, celebrating Christmas here with our family.

The month didn’t necessarily start well. I experienced another bout of pink eye. I was quarantined for almost a week in the room to prevent the kids from getting it. Luckily none of my family members got it. Just after that, Mr. MMD were out of commissioned for almost a week with some cough and chills. At first, I thought it was COVID, but luckily it wasn’t. It still didn’t feel good.

The kids, luckily didn’t get anything aside from some snot and mild cough. At home, they opened their lego Advent calendar and we light up our Menorah for the Chanukah. We put up the Christmas tree, played dreidel and listened to a lot of Holiday Favorites through Alexa. During the start of the break, we drove north and saw the Snowflake Lane in Bellevue. Similar to last year, we made a day out of it and went to Children’s Museum. This year, we also went to a toy store and the boys got something from us. Usually, we eat out at Cheesecake factory, but since this is the first day of the break, it seems that half of Seattle thought the same. We ended up eating an overpriced Greek food inside the mall. AHP was disappointed because he LOVE cheesecake, but luckily he was ok with it. We also got them an overpriced light up balloon, which broke the next day. Now, they know that we will no longer be buying those things next time. I also know to make a reservation at Cheesecake factory next year.

Holiday Craft at AHP’s School

Aside from Holiday festivities, I also attended my book club and started tax training for the upcoming tax season. Similar to last year, I will be managing a tax site and prepare taxes for low income folks. I’ll only be working for 4 hours, 2 days a week. I usually clock in more hours and try to help out during busy times. It was a very rewarding experience. It’s not something that I do for a paycheck, but I do cash it.

MBP’s list for Santa

For this month I will write about our total expenses for the year, instead of our monthly expenses. I’m still getting used to Empower to track our expenses. I’m not sure if I like it, but I’m giving it a try. For this annual expense, I used Mint, probably for one last time.

In total, we spent $81,511.22. We spent 9% more or $7,582.69 more than 2022. I want to say that we loosen up on spending this year, but this is probably more normal. There were one time expenses, like putting up a heat pump but you can say that every year. Our house is 10 years old. I expect that we will need to replace some appliances starting next year. We also spent more on travel this year. We went on Alaskan Cruise and visited almost every theme park in Southern California. This is a lot different than our camping trips in 2022 and significantly more expensive. We also live in a state with high cost of living. Even day to day expenses are just more expensive in general.

Alright, so where did our money went and how did it compare to last year?

CATEGORY

2022 Spending

2023 Spending

Difference

% Difference

Home

$2,126.21

$21,143.00

$19,016.79

894%

Food & Dining

$10,483.75

$11,350.11

$866.36

8%

Travel

$2,405.73

$6,809.96

$4,404.23

183%

Gifts & Donations

$6,114.80

$6,623.83

$509.03

8%

Taxes

$27,224.42

$6,231.80

($20,992.62)

-77%

Health & Fitness

$4,743.79

$6,058.13

$1,314.34

28%

Kids

$5,317.24

$5,851.43

$534.19

10%

Auto & Transport

$3,527.41

$5,323.57

$1,796.16

51%

Bills & Utilities

$4,333.60

$4,163.80

($169.80)

-4%

Shopping

$3,102.42

$3,581.79

$479.37

15%

Pets

$1,620.28

$2,775.09

$1,154.81

71%

Fees & Charges

$954.74

$476.73

($478.01)

-50%

Business Services

$40.56

$444.15

$403.59

995%

Personal Care

$468.92

$399.55

($69.37)

-15%

Entertainment

$1,464.66

$278.28

($1,186.38)

-81%

Total

$73,928.53

$81,511.22

$7,582.69

Home – $21,143

This is the highest category of our spending this year, up by $19,016.79 from last year, an 894% increase. This year, we installed a new heat pump, added a shed in our backyard and bought a new couch, a new latex mattress and a new queen size bed. All of it definitely add up. That said, we also use all of it on a day to day basis. There were some small items we bought this year like 2 apple trees and 3 blueberry bushes. The rest are annual items like home insurance and HOA dues.

Food & Dining – $11,350.11

This is $866.36 increased from last year or 8%. This is not bad, especially since this includes food and dining while we travel. Groceries clocked in at $8,857.27 for the year. We ate out more as well with $1,715.8 spent at restaurants and $541.46 at fast foods. Coffee shops were only $84.52.

Travel – $6,809.96

We spent more on travel this year with an increase of $4,404.23 or 183% increase from last year. Our travel is a little different this year. We went on Alaskan Cruise, which is not the cheapest. We also went to San Diego and visited a ton of theme parks and went back to Disneyland in the beginning of the year. I actually prefer this type of long vacations instead of 2-3 nights camping trips.

Gifts and Donation – $6,623.83

This also increased by $509.03 or a 9% increase from last year. $5k were our annual gifts to my parents and the rest are donations / gifts for Christmas. I do feel more generous this year. We are pretty fortunate, so it is good to share it.

Taxes – $6,231.8

At least our taxes decrease significantly by $20,992.62. We only paid for property taxes. In fact, we received a refund on our 2022 taxes.

Health and Fitness – $6,058.13

Our health and fitness spending increased by $1,314.34 or a 28% increase. I spent $1,183.2 on Eye care. I had a couple of bouts on pink eye last year, which leads to dry eye symptoms. I’m glad it was caught early, but I had a hard time finding an in-network eye doctor. Fortunately, I found one this year, and I’m hopeful that this eye issue will be fix. We were also a member of YMCA for about 9 months last year and spent $1,052.92 this year. We no longer have this membership, but will most likely return during the summer to sign up the boys for swim lessons. Our health insurance were $884.22 for the year. We signed up for a gold plan with a monthly premium of $99.58. We received some “rewards” by getting our annual exam and having some preventative care. We used those rewards to pay for some month’s premium. We just got more rewards which will pay for at least 3 months worth of premium this year. Mr. MMD went back to play hockey. We also have some various doctor payments from various visits with a total of $874.88. We paid more on prescription this year, with the biggest one being my eye drop for my dry eye syndrome. I am hopeful that this will go down eventually with our spending mostly focus on preventative items.

Mt. Rainier view on our daily walk from school

Kids – $5,851.46

This also increased by $1,314.34 or 10%. The biggest one is preschool expenses which is $3,056. We bought a fancy chair for AHP and a fancy bike for MBP. The rest are random items. This is pretty minimal. It might go down once AHP is in Kindergarten, but might also increase since they might be interested on more activities.

Auto and Transport – $5,323.57

We spent 51% more or $1,796.16 this year on our cars. Our 2 cars needed some service this year. The Jetta’s parking break got stuck while the Prius A/C needed some repair. Our 2011 Prius might also need some service this year as it reach 120k miles. This is our everyday car. I’m hoping that we can get another 5 years with this car before we need to get a replacement.

Bills and Utilities – $4,163.8

I’m surprised that this decreased by $169.8. A decrease of 4%. We installed Google Nest this year and a heat pump, so perhaps we are more efficient.

Shopping – $3,581.79

This increased by 15% or $479.37 more from last year. This is just various shopping items, include clothings and electronics.

Pets – $2,775.09

We spent $1,154.81, a 71% increase from last year. Our fur baby had her teeth cleaned and had tooth extract, which is basically the reason of the increase.

Fees and Charges – $476.73

This decreased by $478.01, a 50% decreased. We closed a couple of credit cards with annual fee. We are still earning points. Our flights and hotels in Hawaii for this spring break are all paid by points. I just keep earning, so we should have enough for more trips.

Business Services – $444.15

I spent $403.59 more this year because it is a renewal year for my CPA certification. I also pay for a CPE subscription to get my CPE hours.

Personal Care – $399.55

Some toiletries and haircut.

Entertainment – $278.28

Some games, movies, our state park passes, etc.

We spent more, overall, but nothing extravagant. Unfortunately, I had some eye issue that I’m still dealing with and our healthcare expense seems to be increasing over time. Perhaps, this is a good preview as we age. I’m hopeful that with the right lifestyle, this spending doesn’t increase over time.

We are coming on our 5th year of retirement. I no longer think about going back to work full time. I like the slow paced lifestyle. I still struggle with the gloomy weather and we still haven’t find a community here. COVID of course didn’t help as everyone stay in. I am just now meeting more people through the kid’s school and my book club.

Happy New Year! Here’s to hoping for a great 2024, better health, finding real friends and new experiences.

We had a busy November ending with a nasty germs that took our household. As of today, Mr. MMD is recovering from some nasty cough. A week before I had a pink eye with some mild fever beforehand. The boys also have a never ending snot.

Aside from the germs, we had a good November. We had our annual holiday picture taken this month at JC Penney. I purchased a groupon deal that includes 3 Digital Images and 1 print out. The photographer was really trying to upsell us this time, but I stick with the 3 digital images. It was an easy decision because there weren’t a lot of good images to choose from. The photographer was not very good with the kids. I was lucky to get 1 good family shot.

We also went to the Zoo this month. We got our tickets from Camp Fire. MBP is part of it and they gave out free tickets to the Zoo. They also got a badge by completing some of the scavenger hunt. The zoo already have some lanterns at the time and they are starting to decorate for the holidays.

Visiting the Zoo

The kids also met Santa at the Bass Pro Shop. We got a free photo print out and a “movie”. It is unfortunate that they don’t give out a free digital image. It was my first time visiting the store. It is huge like an REI, but catered more towards hunters, fisherman.

We were also in Central Illinois for 9 days, visiting family. We flew direct to Chicago and drove for almost 3 hours to Bloomington area. The kids are pro at travel by now and did great. In Illinois, the kids were able to run around the corn field, visit the Children’s Museum and spent some quality time with their grandparents.

Visiting the cabin by the lake

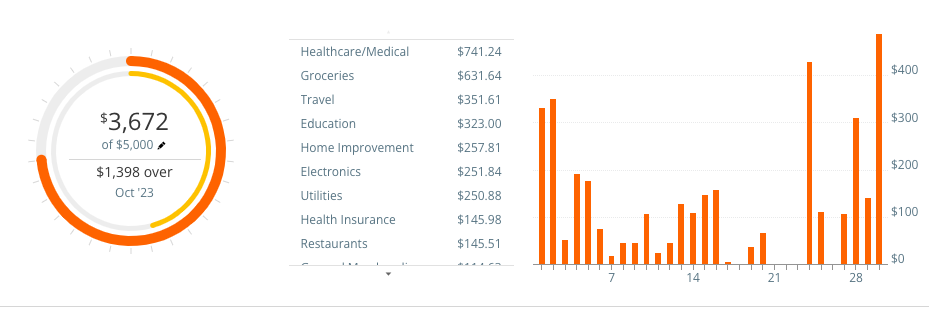

In terms of finances, this month we spent $3,672. This is the first time that our spending was lower than $4k. I also started using Empower, aka Personal Capital to track our spending. I’ve been using Mint for this blog, but Intuit is sunsetting the app, so I’m switching to Empower. We use Empower to track our net worth so all our accounts are there anyway, but it is also more granular on categories. Anyway, here it is…

Healthcare/Medical – $741.24

Mr. MMD had a colonoscopy this month and paid $350 copay. I’m sure there are more bills to come next year or so. I also purchased a transition glasses from Zenni. It was very affordable at $145.24. I’ll write a review after a couple of months of usage. My doctor’s office was about to charge me $400+ for the same glasses. I paid $164 for my eye exam for a new eye prescription. Mr. MMD had a prescription co-pay of $100 after his colonoscopy as well. I also took MBP to an eye doctor to get his vision check. The doctor doesn’t seem concern with his vision. I’m hoping that none of my kids will ever need some glasses.

Groceries – $632

We usually spend $800+ on groceries. This is low because we were visiting family for 9 days and they fed us for free!

Travel – $352

We rented a car through Costco for $349. $4 are for the tolls.

Education – $323

Monthly preschool tuition for AHP. He goes 5 days a week for almost 3 hours.

Home Improvement – $258

I bought 2 apple trees and 3 blueberry bushes to be planted in Spring for $255.31. There is also some charges at Lowes for $2.50

Electronics – $252

Mr. Mmd bought a new monitor for his computer.

Health Insurance – $145.98

Our health insurance is $99.58. Dental Insurance is for $41.4 and my eye insurance is $5.

Utilities – $251

Our gas and electric bill were $137. Sewer were $67 and water were $48. All normal for the month.

General Merchandise – $148

I bought a latex pillow at Latexforless for $75.56 and another slim latex pillow at Amazon for $32.81. I also bought a couple of books at goodwill for our book club book and wine exchange and some bath soap for the boys on subscription from Amazon was delivered this month.

Health Insurance – $146

Our monthly health insurance for $99.58, dental insurance for 41.4 and my vision insurance for $5.

Restaurants – $146

We ate out on our travel days. We also had a take out from our favorite teriyaki place one day.

General Merchandise – $114

This is a catch all of everything else. I bought 2 books from Goodwill for a book exchange for our book club. I also bought 2 new pillows, one from latex from less and another one from Amazon. So far, both are good.

Automotive – $97

This is the annual tab renewal of our 2010 Volkswagen Jetta

Gas – $93

Majority of this were from our trip to Central Illinois.

HOA – $79

Monthly HOA. This will increase to $84 next year

Christmas Cards – $66

I printed out our Christmas cards from Canva. I also got some stamps from USPS and the shipping fee from JC Penney of our Christmas photo.

Gym – $43

I registered for a 5k run here in our neighborhood which will happen in December.

Kids Activities – $35

The kids got some books from scholastic. We also got free tickets from the Woodland Park Zoo, but paid for parking.

Mobile Phone – $17.2

We only used 1 GB of data for this billing.

Pets/ Pet care – $15

I used the Instacart credits and purchased our furbaby her dog food. This is usually $70+.

October went by quick and it was busier than expected. We had our normal October activities like visiting the Pumpkin Patch and Halloween. New this year is MBP fundraising event for his school. It was a school fun run. The school ended up raising $27k+ in this event and MBP’s class raised funds the most. In my opinion, this is a great fundraising event. No need to sell anything, just straight up asking folks for some money. I volunteered at the event and saw the kids had a lot of fun running around. I was initially scared that MBP will need his in-hailer, but he didn’t need to. He did end up crying in the beginning because he keeps tripping while other kids run over him. He was slow. One of the moms saw him and walked him towards me. I told him that he can walk instead, but he insisted on running. The other kids finally slowed down and MBP kept running. He was really focus and was so happy afterwards. I was so proud of him. I’m always worried that his lungs never really develop because of prematurity. He gets winded quickly, but we know that he actually need to slowly develop his lungs through exercise. We walk to school everyday. I’m hoping that this will help.

We picked some Asian Pear at my parent’s house. It’s delicious!

We also visited the Pumpkin Patch this year. We’ve been going here since MBP started in his coop school. I recommended this to MBP’s campfire group. One of the parents put it together and got us a deal, which is fantastic! The weather was great and it was a lot of fun.

Picking Pumpkins

In October we spent $7,982.95. It is less than our September spending. Let’s look at it…

CATEGORY

Spending

Taxes

$3,092.71

Home

$1,429.48

Food & Dining

$1,002.53

Health & Fitness

$833.75

Kids

$407.65

Bills & Utilities

$401.98

Shopping

$392.42

Auto & Transport

$198.11

Uncategorized

$120.00

Pets

$77.32

Gifts & Donations

$27.00

Total

$7,982.95

Taxes – $3,092.71

Our second half of property tax was due. I paid the 50 cents convenience fee to pay via ACH. Washington’s property tax was about 1% of the property value. The rate was actually lower than other state, but property values here in the Pacific Northwest was high, so the absolute value was high. We chose to stay in a “smaller” 2500 sq ft home in our neighborhood. Our house is probably the cheapest in the block.

Home – $1,429.48

I finally bought a new mattress and it cost $1,154.13. We’ve been using my old queen mattress from 2006 and I’ve been having some back issues. It’s been so bad that I slept on our Thermarest Mondo King camp mattress. I actually purchased a king beds in 2019, one from Costco, which we returned and one from Macy’s which we used for a little over a year until it sagged. That Macy’s King Bed was a waste of money. I was hesitant on buying a new mattress again. I spent a lot of time researching. I ended up buying a 9 inch latex mattress with 120 day trial period. I’m on my second week now and so far my back pain is lot a less and I’m back sleeping in the bed. I’ll write a more comprehensive review about it after the 120 days trial.

We also spent $195.7 at Lowes and $79.65 for our HOA.

Food and Dining – $1,002.53

Our groceries clocked in at $958.6. There might be some non-grocery items here since we buy some other things at Walmart and Costco. Now that the boys are in our neighborhood schools, it’s easier to buy groceries at Walmart, but Mr. MMD still go to Winco for the bulk section items. I ate out in the beginning of the month and spent $31.93 and we also got the boys a $12 cotton candy during Salmon Days.

That is a unicorn shape overprized cotton candy

Health and Fitness – $833.75

I continue to see an out of network ophthalmologist. Apparently I suffer from dry eyes. The prescription cost $310 for a 6 month restasis treatment. I saw a chiropractor 3 times this month as well. Total cost of doctor visits were $273.77 for both the opthalmogist and chiro. Our health insurance for a gold plan is $99.58. Our dental insurance were $41.4. I also started a vision insurance for $5/month. I also had a dental filing this month and it cost me $104 for co-pay.

Kids – $407.65

Preschool tuition is still a majority of this at $323/month. Supplies are $54.11 and other school materials are $30.54

Our neighborhood halloween festivities. The kids were scared of these decorations

Bills and Utilities – $401.98

Our electric and gas is $198.78. This is for 2 months as I forgot to pay it last month. Sewer is constant at $66.46. Internet is $61 for 2 months. Water is $46.78. We used about 2gb of data for our cellphone and paid $28.96 for 2 lines.

Shopping – $392.42

Overall shopping is $172.39. Clothing, mostly kids clothes, kids shoes and halloween costumes are $142.33. Household supplies are $70.05 and our prime subscription is $7.65

Auto and Transport – $198.11

Gas were $198.11. and oil change for our 2010 Volkswagen Jetta is $84.3

Misc – $120

Mr. MMD withdrew $120 cash. He likes having cash, which we usually spend at the fair or Sunday market.

Pets – $77.32

Our Corgi’s food.

Gifts and Donation – $27

This is the Groupon deal for our annual family photo that we used for our holiday cards.

We spent quite a bit on furniture this year. I get a lot of utility on these items and everything is use everyday. Our couch is awesome and we use it everyday. Our bed is awesome and we use it everyday. My hope is that our new latex mattress will last like my old queen mattress that I bought in 2006. So far it is comfortable, but it is too soon to tell if it will sag or not. Our shed housed all our garden materials everyday.

Mint is about to sunset and I will be moving our spending to Empower going forward. There are 2 more months left in 2023. Holidays are in full swing. I’m looking forward to it.

School started for both kiddos. For the first time in many years, the house was quiet for a couple of hours in the morning. It was a little weird not having the kids at home, but it is nice to do have some time to actually do some work.

We continue to do some work around the house this September. We, really means Mr. MMD. In September, he finished putting up the shed and put the insulation back in our crawl space. Apparently, a big chunk of the insulation fell to the ground because nothing is holding it up. Mr. MMD, managed to fixed this. Hopefully, it will stay put. Other household project includes buying a bed frame for us and a new couch. I led this project and you can see this on our spending.

I used the morning time to organize and declutter. We finally got rid of the grass fertilizer and other household chemicals that were in the laundry room. Funny that we actually move those items in our new house and it took us 4 years to get rid of them. I donated some clothes and household items in Goodwill. Decluttering is really a never ending project, especially with the kids stuff.

AHP finally let go of this trampoline Time for other kids to have fun with it!

I also had my eye examined by an ophthalmologist. It was so hard to find a doctor in my network that I actually went out of network. I’m just glad that I was seen and I’m hoping that this issue will get fix. I also started going to a Chiropractor. I started having some lower back issue when we switch mattress. I’m still having some and I’m looking for a new mattress. My insurance covers 10 visit with a $15 copay per visit. I like my insurance for that and I also like my chiro.

In September, we spent $11,691.21. This is huge and we are living large! I wish I can say that our spending will go down, but I can’t see this happening. We will re-asses by the end of the year. We might need to put together a budget if our spending continue to increase. Let’s take a look where we spent our money.

CATEGORY

Spending

Home

$5,937.62

Pets

$1,564.17

Kids

$940.82

Food & Dining

$809.39

Travel

$791.20

Health & Fitness

$651.45

Auto & Transport

$622.72

Shopping

$164.31

Bills & Utilities

$126.81

Personal Care

$75.44

Gifts & Donations

$7.28

Total

$11,691.21

Home – $5,937.62

The biggest items are furnishings. Mr. MMD and I haven’t bought a new furniture together. Our couch is falling apart and I’d like to have a real bed. Macy’s had a sale for labor day and we spent $3,735.04 on a sectional and a queen bed. The amount included a $299 white glove delivery. The guys came in and assembled the furnitures and took out all the garbage with it. It’s well worth the price. I listed our old couch and love seat on our buy nothing page and it was picked up the next weekend.

Goodbye Old Couch. You served us well for 14 years

We also purchased our shed at Walmart for $1,289. We received a $12 credit from Chase offers by ordering on Walmart online. I also got a couple of clocks for the playroom and the living room, a dozen new glassware, flatware for MBP’s lunch box and some scissors at Ikea. I used some old gift card and spent $48.30 on the balance.

The shed with our planter on the left and heat pump on the right

The next item under home, are Home Improvement. These are the expenses to prepare the ground for the shed. Mr. MMD rented a tamper to even out the ground. The cost is $343.51 with delivery. He also ordered some gravel which cost $307.7. We spent $146.42 for various visit at Lowes.

Last category for home is our HOA fee for $79.65.

Pets – $1,564.17

This is a fee for our furbaby’s tooth extraction and tooth cleaning. This is her second tooth cleaning since we got her and is totally overdue. Our dog doesn’t like her teeth brushed. The vet needs to give her some anesthesia for it.

Kids – $940.82

We spent $350.31 on Kids Gadget. We moved AHP out of his high chair and got him a Stokke Chair. I’ve been looking for a used one for months, but I think kids uses it for so long and I never saw a used one closed to us. I didn’t want to drive too far so I hit the buy button at Amazon, instead. It’s expensive at $261.71, but the kids are using this chair everyday. MBP’s chair is still going strong after 3.5 years of use. This is one of those items that I think is worth the splurge for our family. I also got MBP a lunch box. The price is steep at $49.22 but MBP seems to really like it. We can pack hot lunches with it from our left over dinner. The box is big enough to hold his lunch and afternoon snack. I also got AHP a new backpack for his preschool, a headphones for MBP and a rain shield for our double umbrella stroller. We’ve been walking to and from school everyday. The walk is .7 miles one way with elevation of 115 ft. He can walk to school but struggle going back because of the hills. I pick him up with the double stroller. He’ll walk until he gets tired and will climb into the stroller.

Preschool tuition for AHP is $323. We spent $176 on various kids activities. I signed up MBP for Camp Fire. It’s an after school activity that meets every other week, completely ran by parents. The fee and the vest is $78 for the year. I also paid $68 for their school photos and $30 for the pumpkin patch, which happened in October.

School is $91.51. These are various expenses related to kids school like, PTA membership fees for $20 and teacher wish list donation for the rest.

Food and Dining – $884.88

We spent $842.10 on groceries. Mr. MMD spent $38.36 for dinner with his buddy and I spent $4.42 for coffee. We actually didn’t eat out this month.

Travel – $791.2

We bought 4 tickets to Chicago to visit my in-laws for Thanksgiving. I booked a rental car from O’Hare Airport through Costco to drive to Bloomington area. There were plenty of direct flight to O’Hare from Seattle and it makes more sense to just drive to Bloomington instead of flying there.

Health and Fitness – $651.45

I’ve been having some eye issues since June. I can’t find an in-network ophthalmologist on my insurance so I went out of network. I really like my doctor and I’ll be switching to her next year. The cost of my first visit was $266.47. I also paid $30 co-pay for my 2 visits at chiropractor. We paid $154 for our YMCA membership. We never really went to the Y this September, so it will not be a recurring expenses for us until next summer. Our health insurance was $99.58 and our dental insurance was $41.40. I also paid a $50 co-pay for my dentist. Lastly, I paid $10 co-pay for my eye drop. This eye drop cost over $100 without insurance. We are definitely using our insurance this year.

Auto and Transport – $625.96

Our 6 months auto insurance was $534.37. This is for our 2010 VW Jetta and 2010 Toyota Prius. We also spent $79.55 on fuel and $8.8 on tolls from this summer.

Bills and Utilities – $126.81

This is for our water at $43.39, sewer at $66.46 and mobile phone at $16.96. We are back on consuming 1GB on our Xfinity Mobile.

Shopping – $123.31

We got MBP the Super Mario Odyssey game for his switch. He is almost done with it and is now on the bonus section. The cost is $58.2. I also got him a pair of rain boots / snow boots for $43.77. This is a must in the Pacific Northwest. I spent $13.69 at Dollar Tree for sticker books and we also paid $7.65 for our prime subscription.

Personal Care – $40.95

The boys had a hair cut. This is actually cheaper because our hairdresser have a 1 free hair cut for every 10 hair cut. It’s usually cost us $60+ including tips.

Gift and Donation – $7.28

We went to AHP’s friends birthday party and this is the boy’s gift to her.

We wrapped up our Summer Adventures, visiting Southern California. We were there for 11 days, visiting Legoland, San Diego Safari, San Diego Zoo, Seaworld, the Aquarium and Belmont Park. Hurricane Hilary were there during our last days and our planned beach days were canceled. San Diego closed the public beaches during that time. We stayed in our hotel instead.

Checking out the Ninja Lego in Legoland

Back to school activities started once we were back home. MBP had quite a bit of friends meet ups with upcoming kindergarteners. There were donut days, sweet and treats days and cookies and milk days. It was fun meeting families in the neighborhood. After 4 years of living here, we are finally meeting getting to know our neighbors.

We continue to loosen up on spending. In August, we spent, $4,840.75. I’m just seeing this the first time too, so let’s dissect our spending.

CATEGORY

Spending

Travel

$1,452.00

Food & Dining

$1,242.73

Bills & Utilities

$519.78

Home

$452.24

Health & Fitness

$338.96

Auto & Transport

$288.78

Shopping

$274.18

Kids

$184.62

Pets

$77.32

Personal Care

$8.41

Fees & Charges

$1.73

Total

$4,840.75

Travel – $1,452.00

This cost is associated with our travel to Southern California. Our flight tickets, 9 nights of hotel stays and car rental were paid with points. This is mainly for activities. First, I bought 2 adults and 2 kids 7 day San Diego Go City all inclusive pass. This pass let us visit Legoland 3 times, San Diego Safari, San Diego Zoo, Seaworld, Aquarium and Belmont Park all inclusive rides. I priced out these passes against the cost of individual tickets and it was about a couple of hundred cheaper even though we didn’t visit a lot of places. We would have saved more if we added more activities, but the point is to have a relaxing trip. I bought the passes at Groupon for $1191.88.

We also bought 2 travel car seats at Walmart for $107.08. Our car seats were heavy and we didn’t want to haul it all the way to San Diego. We did it on our last trip in Chicago and vow that we will not travel with those car seats again. We spent $94.01 for hotel parking and some ice cream in the hotel lobby. For these trips we stayed at 3 different hotels – a Hyatt Place, Hyatt House and Fairfield Inn Marriott. I redeemed my Ultimate Rewards from Chase to book the Hyatt hotels and spent $51.03 at Fairfield for one night before our departure. The Fairfield rate is a family member employee rate through my father. We also spent $8 for some knick knacks at Seaworld San Diego.

San Diego Safari. It was hot!

Food and Dining – $1,242.73

This is expectedly high since we ate out more while traveling. We still brought our rice cooker and made some dinner in the hotel. We did groceries and pack some lunches and snacks as much as we can. We spent $667.4 for groceries for the month. The restaurants that we visited were actually really good and I was very impressed. We spent $445.85 on restaurants and $129.48 on foods in the theme parks, fast food and trip to get frozen yogurt back here at home.

Utilities – $519.78

We spent $189.31 on electric and gas. This was for 2 billing cycles. Our garbage bill also charged me for 2 billing cycles and cost us $162.48. We now have a credit on our account. Sewer is flat at $66.46. Our water boll is $51.57. Internet is at $33 and our phone is back at $16.96.

Home – $452.24

This category will also continue to go up. We started a list of home projects. We will take our time, so the cost will not be one time. Majority of the work will also be a labor of love my Mr. MMD, so it shouldn’t be that high. This month we spent $372.59 with 4 charges from Home Depot and 2 charges from Lowes and 2 charges from Amazon. Mr. MMD is almost done with putting the gravel in our yard for the foundation of our shed. It looks nice right now even without the shed. Our HOA is flat at $79.65

Health and Fitness – $338.96

Our health and dental insurance were $281.96. This was also for 2 billing cycles. I paid for a copay of $35 for an urgent care visit that happened last June.

Shopping – $274.18

We renewed our Costco membership for the year at $120. We are now an executive member. We shop there so often that we will get this back in terms of cash back for the year. My 20 year old hair dryer also stopped working. It just stopped heating up. I bought a CONAIR hair dryer from Amazon and cost $33.59. We spent $29.01 on household supplies, $29.01 for MBP’s new Kirby backpack and lunchbox, $10.72 for a souvenir in San Diego Zoo and $7.65 for Amazon subscription.

Auto and Transport – $288.78

We spent $178.78 on gas, including gas to our rental car while we were in Southern California. Gas price there is comparable to Seattle. We also spent $110 on parking at the theme parks that we visited.

Kids – $184.62

Kids activities are $100 fro a visit to Chuck E Cheese and school supplies for MBP’s Kindergarten. Diaper cost us $44.99. We also bought Super Mario Cart Game for $39.63.

The Dolphin show is pretty cool

Pets – $77.32

Our furbaby’s food. She will also need to get her teeth clean and a tooth extract. So this category will be high next month.

Personal Care – $8.41

Kid’s shampoo. How exciting!

Fees and Charges – $1.73

Fee for a credit card interest that I forgot to auto pay. Oh well.

The kids are now back to school. This is the first year that both of them are out of the house for a good half a day. It just started and AHP already caught a cold and had a fever. He missed 2 days of school on his first week. I’m really hoping the we don’t get hit by a bug as frequently as last year. That said, with them being gone, we have more time to ourselves. I still don’t know what it looks like but I’m looking forward to it.

We spent July at home and enjoyed the great weather in the Pacific Northwest. We were invited to a pool party during 4th of July and to a private lake spot. We definitely enjoyed all of those, though for a moment, I thought about stepping up our game and host something just as elegant, gladly we were out of there right away.

We hit the beach on one of the days

My in-laws also had their annual visits and we all had a great time. It was very laid back and we stayed local. The boys were over the moon.

Mr. MMD and MBP paddle boarding

This month, we started some housework that was put off for the last 4 years. There were some work we wanted to do at home when we initially bought our house. We put it off because we thought we were going to move. After 2 years of searching with a dozen house visits, we finally decided that we will stay put.

So for this month, we spent $13,738.58. The spending trend this year is up, up and up. I wonder if this will be a new normal.

CATEGORY

Spending

Home

$11,640.79

Food & Dining

$749.49

Shopping

$355.80

Fees & Charges

$285.00

Health & Fitness

$274.74

Bills & Utilities

$258.80

Auto & Transport

$60.83

Pets

$38.26

Entertainment

$35.00

Kids

$20.88

Personal Care

$18.99

Total

$13,738.58

Home – $11,640.79

After 21 years of living in the Pacific Northwest, I am finally living in a house with central A/C. We installed a heat pump in our house. We actually thought about getting central air 3 years ago after a year of living in our house. The initial quote then was about $7k. Once we decided to stay put, I know that it’s time to install a central air, in case we hit another 90+ degree weather. We spent $10,507.86 for a heat pump. So far, we haven’t had the need to turn on the A/C. We keep it at 75 and our house has been cooler than that.

Since we are staying put, we also decided to add a shed in our backyard. The initial work happened this month, which consist mostly of digging our very rocky land. Mr. MMD did almost all the work. There’s no shed yet and it will probably take another month or 2 before it’s there. I would say, I’ll be happy if we can actually finish a project this year, then we can move on and do some projects inside the house. We spent $121.9 at Home Depot for some wood and some tools.

We also paid our annual Home Insurance at Nationwide for $931.37. I paid it at 4th of July, hoping that our house don’t get burn by the neighborhood fireworks.

Lastly, we paid, $79.65 for HOA Dues.

Neighborhood Fireworks

Food and Dining – $811.86

Our grocery bill is at $637.21. This is low this month. My in-laws were here and they paid for grocery and restaurant for 10 days that they were here. We spend $800sh on average. We spent $162.62 on restaurants. We paid for one take out meal with my in-laws. I met up with a friend and had some ramen and a couple of bubble tea. I only drank one Taro bubble tea and got another one to go for the kids. MBP really enjoyed it. We also ate out and had some Dimsum. Lastly, we got a large kettle corn at the local farmer’s market.

Fees and Charges – $285

This is for 3 Annual Membership Fee for 3 credit cards. We opened 2 Chase Ink Business Preferred in anticipation of paying our heat pump. We already got one sign up bonus of 100,000 points. I value this at about $1,500 conservatively. I’m ok paying for these fees, because we get more value from the sign up bonuses.

Health and Fitness – $274.74

Our monthly YMCA membership is $154. The boys have been taking swim lessons at the Y. MBP is doing really well and AHP is getting more and more comfortable with the water. We were also able to take our in-laws and they swam with the kids at the Y. Mr. MMD also paid $120.74 to play hockey for the season.

Bills and Utilities – $258.8

We paid $112.82 on our phone bill. Mr. MMD used quite a bit of data that month and it actually surprised both of us. Our monthly sewer bill is $66.46. Our water is $59.52 and our internet is at $20.

Shopping – $226.10

Shopping is a catch all. It’s clothes, housing supplies and prime subscription

Auto and Transport – $60.83

We filled up twice and paid 50 cents of parking in Seattle.

Pets – $57.81

Food and treats for our furbaby

Our Corgi watching the fireworks

Kids – $57.66

I bought the kids 2 headphones for travel. I also bought a travel stroller from our neighbor.

Entertainment – $35

Our Annual Discover Pass to visit the state Parks in WA. We already visited 2 state parks this summer.

Personal Care – $29.99

Not sure why Mint is not categorizing it as shopping, but these are just toiletries.

That’s our July. We spent half of August in California. I’ll talk about that on the next month’s update.